Much has been written about IRC Section 1202.[1] Section 1202 affords non-C corporation taxpayers who sell a corporation’s qualified small business stock (“QSBS” or “1202 Stock”) issued after July 4, 2025 (and who satisfied the holding period requirement) a gain exclusion from federal income tax for QSBS sold in a taxable year equal to the greater of: (1) 10x their tax basis in such transferred stock, or (2) $15 million (reduced by the aggregate amount of prior gain exclusion).[2]

Because of the significant tax savings, it is critical for taxpayers to engage qualified counsel early in the QSBS planning process to assist with qualification, substantiation and penalty avoidance, and if the investment proves successful, to help them maximize the amount of gain exclusion.[3]

This article introduces Section 1202’s requirements and focuses on maximizing QSBS tax benefits through: (1) stacking QSBS gain exclusions and (2) staggering sales over multiple tax years. Tax professionals rarely discuss the strategy of staggering sales of QSBS over multiple tax years, but this strategy is beneficial to founders of corporations where such persons have multiple blocks or classes of 1202 Stock, each with a different tax basis (e.g., where a founder owns both founder common stock and preferred with a significant tax basis). Further, staggering can prove to be particularly useful where founders and other stockholders are participating in secondary sales.

1. General Section 1202 Requirements

General Section 1202 requirements include:

- Original Issuance. The 1202 Stock gain exclusion is only available for originally issued stock by a C corporation.[4] It can be important to know the difference between permissible transfers (e.g., gifts, distributions of QSBS by a partnership to a partner, and “at death” transfers) and impermissible transfers of 1202 Stock, especially in the context of partnerships because permissible transfers allow the transferee to become a qualified holder of QSBS.[5]

- Holding Period. For a 100% gain exclusion (subject to the caps discussed earlier), the taxpayer must have at least a five-year holding period in the QSBS sold or exchanged.[6]

- Active Business Requirement. The issuing corporation must use 80% of its assets (measured by value) in the active conduct of one or more qualified trades or businesses.[7] Taxpayers holding QSBS must satisfy this 80% test (among others) for “substantially all” of their QSBS holding period.[8]

- Qualified Trade or Business. The issuing corporation must engage in one or more qualified trade or business activities. “Qualified trade or business” means active trade or business activities other than:

- any trade or business involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of 1 or more of its employees. . . [Emphasis added; also see below for a more complete list of non-qualified trades or businesses].[9]

Note that Treasury Regulation § 1.199A-5(b)(2)(xiv) appears to limit the definition of a trade or business where the principal asset of such trade or business is the reputation or skill of one or more employees or owners to endorsement fees, fees attributable to licensing image, likeness, name, etc., and appearance fees.

- Gross Assets Test. All times before and immediately after the issuance of the applicable stock, the corporation’s “aggregate gross assets” cannot exceed $75 million.[10] Once the test is satisfied, the corporation’s aggregate gross assets can exceed $75 million without adversely affecting the QSBS status of outstanding stock. [11]

Each of these tests has nuances. For example, S corporations can terminate their election or contribute assets directly or indirectly to a C corporation and the C corporation can then issue QSBS. [12] But gain associated with appreciation in assets prior to those assets being held by a domestic (U.S.) C corporation will not later qualify for the QSBS gain exclusion.[13]

2. Maximizing 1202 Stock Benefits

A. Stacking Exemptions

Permissible transfers of 1202 Stock include gifts to non-grantor trusts. Gifting 1202 Stock to non-grantor trusts is a way of increasing or “stacking” 1202 Stock exclusions.[14] This works because the Code typically treats non-grantor trusts as separate taxpayers for Section 1202 purposes. So, a founder or early investor who has or anticipates having children may transfer QSBS to a non-grantor trust, and as a separate taxpayer, the Code entitles the trust to its own separate QSBS gain exclusion.[15]

The timing of a taxpayer’s gift to the non-grantor trust is important for gift tax considerations. An earlier gift (say, during year 1) of 1202 Stock to a non-grantor trust may result in a smaller valuation than a gift in year 5 or year 6 when multiple potential buyers are bidding up the price of the 1202 Stock. Therefore, making the gift of 1202 Stock shortly after formation could potentially maximize both wealth transfer planning and federal income tax benefits.

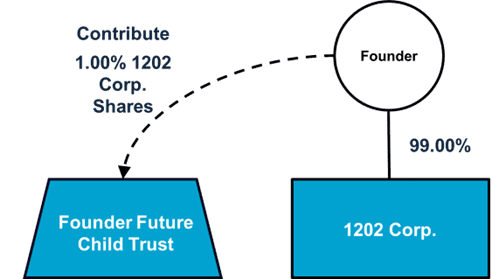

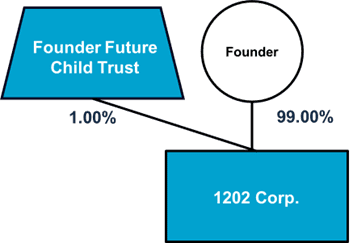

For example, an individual taxpayer (the “Founder”) who owns 100% of the QSBS of a corporation (“1202 Corp.”) could, prior to entering into a binding sale agreement, (i) form a non-grantor trust for her child, (ii) gift shares to the trust, and (iii) later, both the trust and the Founder could sell the 1202 Stock and separately qualify for the Section 1202 gain exclusion. The following depicts these steps (excluding the sale) as it relates to a non-grantor trust (the “Founder Future Child Trust”):[16]

| 1. Beginning Structure | 2. Formation of Trust |

|

|

| 3. Contribute 1202 Corp. Shares to Founder Future Child Trust | 4. Ending Structure |

|

|

What Is the Benefit of Stacking?

When the Founder Future Child Trust and the Founder sell shares in 1202 Corp., both the Founder Future Child Trust and the Founder can each exclude at least $15 million of gain from the sale of QSBS.[17] After the sale, the Founder Future Child Trust can use the funds for the benefit of the Founder’s current or future child.

Tax planning does not stop if the Founder or the Founder Future Child Trust sells 1202 Stock. When using trusts to stack 1202 Stock benefits, parties must consider how to use the proceeds of the sale to further estate planning goals. While most states have 1202 Stock benefits similar to the federal rules, taxpayers must consider state law when deciding where to set up a trust. Some states have a state income tax that will meaningfully affect investment returns from 1202 Stock proceeds. Furthermore, different states have different laws regarding creditor protection, the ability to decant and modify trusts, and trust and beneficiary privacy. For example, it would generally not make sense to set up a trust under New York or New Jersey law when some states, such as Wyoming, are objectively superior for long-term wealth planning and protection.

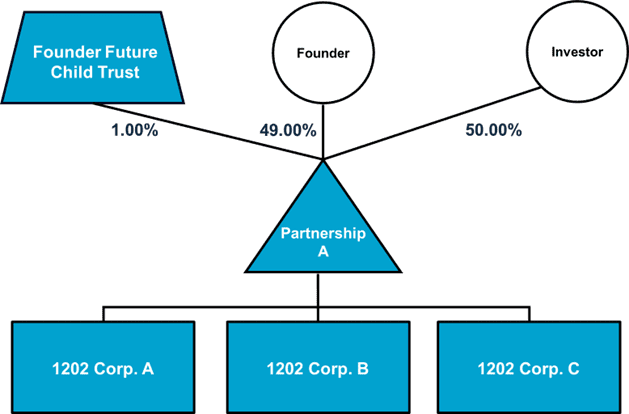

Multiple 1202 Corporations?

Where the Founder has formed a partnership with a financial backer (say, an LP), and that partnership intends to make several investments in QSBS — each possibly qualifying for Section 1202’s gain exclusion — the Founder could gift interests in the partnership prior to the partnership acquiring 1202 Stock. In this scenario, a QSBS gain exclusion would be available for each of the corporations subsequently formed or acquired by the partnership.

The final structure would be as follows:

*Assume Partnership A owns 100% of 1202 Corp. A, 1202 Corp. B, and 1202 Corp. C.

When Partnership A, in the diagram above, sells the stock of 1202 Corp. A, 1202 Corp. B, or 1202 Corp. C, the Code entitles both the Founder Future Child Trust and the Founder to a separate gain exclusion for each separate QSBS investment because they are separate taxpayers. This may be simpler and more efficient from a gift-tax perspective than contributing each entity’s stock to the Founder Future Child Trust.

With some advanced planning, the Founder could have Partnership A issue profits interests to key employees of 1202 Corp. A., 1202 Corp. B, or 1202 Corp. C (or, imposing a lower-tier partnership between Partnership A and each 1202 Corp.). The holders of these profits interests should qualify for 1202 Stock gain exclusions assuming they acquire such interests prior to Partnership A (or a lower-tier partnership) acquiring the QSBS. Another approach that is cleaner from a tax perspective is for the corporation to issue incentive equity directly to key employees.

B. Staggering Exemptions

This section explores how the Founder can stagger the sale of 1202 Stock over two or more tax years to potentially maximize the amount of the Founder’s QSBS exclusion.[18] This technique should be particularly useful if the Founder holds both “cheap” founder common stock and more expensive preferred stock acquired in a later capital raise, or in the situation where there is only one class of stock, but the Founder has multiple blocks with different tax bases.

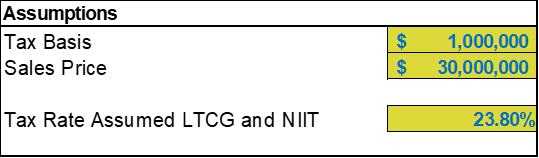

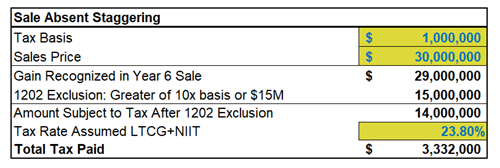

Assume that the Founder owns all of 1202 Corp. (similar to the Beginning Structure above) with a $1 million aggregate tax basis and a six-year holding period.[19] Further assume the Founder participates in a secondary sale by selling all of her QSBS. Assume the sales price for the Founder’s QSBS is $30 million.

If in year 6, the Founder sells her entire holding, the gain calculated is $29 million (sales price less tax basis). Of such gain, Section 1202 excludes $15 million (the greater of 10x basis ($10 million) or $15 million), leaving $14 million subject to taxation at U.S. federal long-term capital gains tax rates, plus the net investment income tax (“NIIT”) (plus applicable state and local taxes).[20]

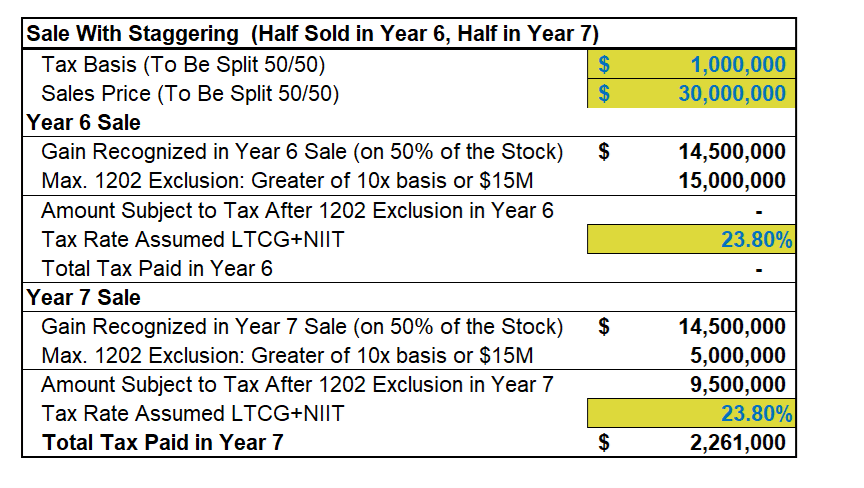

If instead, the Founder sells 50% of her QSBS in separate secondary sales in two separate tax years, using the staggering technique, the approximate tax consequences (using the Assumptions table above) are as follows:[21]

- Year 6 Gain (Without Section 1202’s Benefits): $15 million sales price less $0.5 million tax basis = $14.5 million gain.

- Year 6 Gain Using Section 1202: Exclude all gain from this sale using the $15 million exclusion amount (which is greater than 10x tax basis ($10 million)).

- Year 7 Gain (Without Section 1202’s Benefits): $15 million sales price less $0.5 million tax basis = $14.5 million gain.

- Year 7 Gain Using Section 1202: Exclude “10x basis” from gain on this sale because applying the 1202 gain exclusion, 10x basis of $500,000 ($5 million) is greater than $0.5 million remaining of the applicable dollar limitation of $15 million ($14.5 million was used in year 6). Accordingly, $5 million of the year 7 gain of $14.5 million is excluded.

Using this staggering strategy, the Founder is taxed on $9.5 million of capital gain, rather than $14.0 million of capital gain had the Founder sold the stock in one tax year:

Accordingly, when the Founder uses the staggering technique in our example, the Founder (or any selling stockholder that satisfies Section 1202) pays approximately $2.26 million in U.S. federal income tax instead of the $3.3 million in U.S. federal income tax she would have owed without staggering. The Founder is able to save approximately $1.1 million in after-tax cash through careful planning and assuming tax authorities respect the multi-year sale.[22]

With careful planning, owners of QSBS can increase the amount of tax savings on the disposition of their QSBS. Stacking and staggering 1202 Stock exclusions and sales accomplishes this goal. The use of non-grantor trusts can provide a useful tool in stacking 1202 Stock exclusions, as does early tax structuring to ensure that LPs, founders, and even profits-interest holders are in a position to maximize the Section 1202 gain exclusion. Federal income tax planning should be coordinated with the taxpayer’s estate plan and a careful eye on what also works best from a wealth transfer planning standpoint.

Should you have any questions or comments on these topics, please contact the authors or any attorney with the firm’s Tax Practice Group. You can also visit our Tax Law Defined® Blog for more insight into the latest developments in federal, state and local tax planning and tax administration.

[1] The information provided in this article does not constitute legal advice and does not create an attorney-client relationship. References to “Code,” “Section,” or “IRC” are to the Internal Revenue Code of 1986, as amended.

[2] See generally I.R.C. § 1202(a), (b). Amended I.R.C. § 1202 provides a 50% gain exclusion for QSBS held for at least three years, a 75% gain exclusion for QSBS held for at least four years, and a 100% gain exclusion for QSBS held for at least five years. I.R.C. § 1(h)(4)(A)(ii) generally taxes the portion of the gain not eligible for exclusion at a rate of 28%.

[3] Accuracy penalties (excluding interest) can be 20% of the amount of underpaid taxes. See I.R.C. § 6662. Interest accrues on the tax due and the penalty from the date payment was due, and for individuals is 3% plus the federal short-term rate, calculated quarterly and compounded daily. See I.R.C. §§ 6601, 6621.

[4] See I.R.C. § 1202(c). For example, typically, if Individual A purchases the 1202 Stock from Individual B, then Individual A cannot qualify for QSBS benefits upon a subsequent sale by Individual A because the 1202 Stock was not originally issued to Individual A.

[5] See I.R.C. § 1202(h)(2). In the partnership context, the form of a transaction is critical.

Example (Impermissible). As an impermissible transfer, if an individual first acquires 1202 Stock directly and then contributes it to a partnership in exchange for a partnership interest, neither the partnership nor the individual will qualify for the gain exclusion under I.R.C. § 1202. The individual should have simply retained the 1202 Stock and sold it herself.

Example (Permissible). A permissible transfer exists when a partnership distributes the 1202 Stock to a partner.

Lastly, and while not necessarily a transfer, if a partner holds an interest in a partnership, and that partnership acquires QSBS (that is, the partnership is subsequently issued 1202 Stock from a C corporation after the partner has a partnership interest in the partnership), the partner will qualify for the 1202 exclusion upon sale if all requirements of 1202 are met, even though the corporation did not issue the shares directly to the partner.

[6] The One Big Beautiful Bill Act added partial gain exclusions for QSBS held for at least three or four years.

[7] See I.R.C. § 1202(e)(1).

[8] See I.R.C. § 1202(c)(2).

[9] See I.R.C. § 1202(e)(3) (excluding from a qualified trade or business, in addition to the items mentioned, any banking, insurance, financing, leasing, investing, or similar business, any farming business (including the business of raising or harvesting trees), any business involving the production or extraction of products of a character with respect to which a deduction is allowable under section 613 or 613A, and any business of operating a hotel, motel, restaurant, or similar business); see also, I.R.C. § 1202(e)(7) (excluding many real estate businesses).

[10] See I.R.C. § 1202(d).

[11] Id.

[12] Other types of entities or individual taxpayers can also form new C corporations and may be able to contribute assets to such C corporation and start the holding period for newly (and originally) issued 1202 Stock.

[13] See I.R.C. § 1202(i).

[14] See I.R.C. § 1202(h)(2).

[15] The beneficiary of a non-grantor trust generally cannot be the grantor.

[16] This article includes tax shapes to help depict what is happening. See Appendix 1 for a key of what each shape means.

[17] For this article and examples that follow, we assume 1202 Stock was issued after July 4, 2025, and subsequently held for five years because the One Big Beautiful Bill Act (among other I.R.C. § 1202 changes) increased the applicable dollar limit for QSBS issued after July 4, 2025, to $15 million from $10 million, See I.R.C. § 1202(b)(1), (4).

[18] See Scott Dolson, Maximizing the Section 1202 Gain Exclusion Amount, Tax Law Defined Blog (Nov. 12, 2019), (https://fbtgibbons.com/maximizing-the-section-1202-gain-exclusion-amount/ ); see also Gregg Polsky & Ethan Yale, A Critical Evaluation of the Qualified Small Business Stock Exclusion, 42 VA. TAX REV. 353, at p. 371 (Spring 2023).

[19] This example could also apply to an investor owning a percentage of 1202 Corp. or an employee with vested units that meet the holding period requirement in 1202 Corp.

[20] All dollar amounts in this article and any charts herein are in USD. Calculations, applications of law, and analyses are for illustrative purposes only and cannot be relied upon as tax or legal advice, and do not create an attorney-client relationship.

[21] Again, we assume that the seller (Founder, an employee, or an investor) is a calendar-year taxpayer and would sell 50% of the QSBS in year 6 (December) and 50% in year 7 (January).

[22] Again, all amounts are approximations in USD and assume a U.S. federal income tax rate of 23.8% comprised of the highest long-term capital gains rate and the NIIT. For simplicity, we did not depict state income taxes.