This article explores several tax and non-tax considerations that a shareholder (“Shareholder” or “Seller”) should evaluate when selling a business operated through an S corporation (the “Company” or “Target”) for U.S. federal income tax purposes.[1] There are a number of different structures available. These different structures can result in very different tax implications for sellers and buyers and carry with them different corporate law effects.

Owners who wish to sell their S corporation are strongly advised to engage a qualified tax professional who regularly advises on such transactions as early in the deal process as possible.[2] While M&A buyers often end up dictating the structure of an acquisition, Sellers need to have a good understanding of the tax implications of various structures so as to negotiate on a level playing field.

The Parties

For simplicity, assume the buyer (“Buyer”) of the Company (or the Company’s assets) is a C corporation wholly owned by an entity classified as a partnership (“Parent”). Also assume that the purchase price is entirely cash up front (so no deferred payments or earnouts) and that no rollover interests will be retained or acquired by Seller. Admittedly, in most deals today, Buyers will want the Seller individuals to not only work as employees after the business sale for a couple of years, but to also maintain an equity interest directly or indirectly in the Target. Often, Sellers are asked to contribute some of the target stock to a Buyer or its Parent entity in exchange for interests in the Parent as part of the consideration. If done carefully, such exchange can often be structured so as to not be taxable to the sellers.

Should You Sell Stock or Assets?

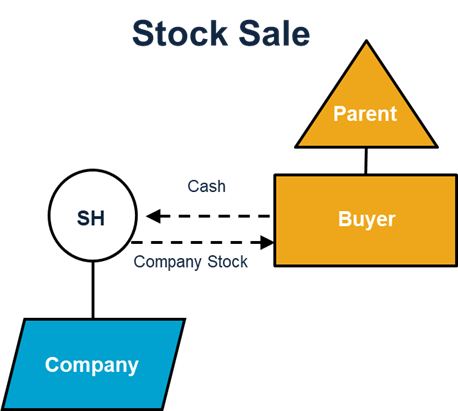

Sale of Stock

Our model Shareholder, like all sellers, for legal and for tax purposes, will want to sell stock in the Company.

One major reason for this is that all legal and tax liabilities of the Company will by operation of law become the indirect obligations of the purchaser (subject to any contractual indemnification provisions in the stock purchase agreement).

From our Seller’s tax perspective, a sale of the Company’s stock is efficient. [3] Shareholder recognizes gain under IRC Section 1001 to the extent purchase price consideration (e.g., cash paid plus outside liabilities assumed) exceeds Shareholder’s tax basis in the Company’s stock.

Assuming that the one-year holding period is met, such gain should qualify for long-term capital gains treatment and be taxed at long-term capital gain rates of up to 20% under IRC Section 1(h). The additional net investment income tax (“NIIT”) of 3.8% can apply under IRC Section 1411.[4] Many states (like New Jersey and New York) will impose income tax on the sale of stock at the state’s normal tax rates (without a favorable long-term capital gains tax rate being available) for the sale of stock.

But what about Buyer? Buyer does not want to assume the possibly unquantified tax or other liabilities of the Company, which Buyer would expressly do if it acquires the Company’s stock.[5] In a stock acquisition, Buyer receives tax basis in the acquired shares equal to the purchase price paid (cost basis under IRC Section 1012). But the stock purchase does not increase Buyer’s tax basis in the Company’s assets.

As such, Buyer does not receive a step-up in tax basis to offset the Company’s income post-acquisition with tax depreciation and amortization. The stepped-up tax basis can be a critical component of providing after-tax cash to certain buyers and is often a critical deal point. For these reasons, Buyer prefers to acquire assets.

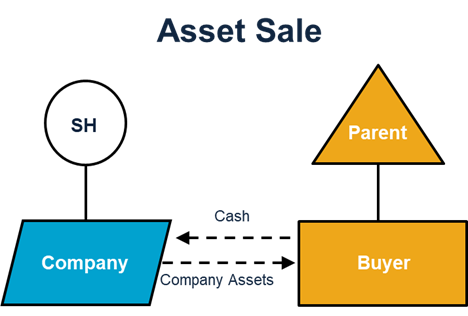

Sale of Assets

If the Company sells assets to Buyer, then the Company will recognize gains (and possibly losses) on such sale of each asset, and such gains (and losses) will flow through to Shareholder, who will pay tax on such gains (i.e, there is one level of tax on the gains).[6]

The character of the gains on such assets is determined at the corporate level. This characterization remains as the gain flows to the Shareholder’s Schedule K-1 and 1040.

Gain on the sale of non-capital assets as defined in IRC Section 1221 (such as accounts receivable, inventory, and depreciation recapture), will be taxed at ordinary income tax rates to the Shareholder, which can reach as high as 37% for individual U.S. federal income tax rates.[7] State tax rates would also apply, (i) to the extent the Company’s business assets are located in a particular state, and then (ii) to the extent that the Shareholder lives in one of many of the states that imposes its own individual income tax (with a credit for the state tax paid to other states).

Fortunately, and due to recent tax-law changes, our Shareholder can mitigate some of the tax burden by making a state pass-through entity tax election (“PTET Election”) in the applicable states that provide for this.[8]

This allows the Company to pay an entity-level state tax on its income (i.e., here, from the sale of its assets), which generates a credit for the Shareholder’s individual state tax return for approximately the amount of PTET paid. Critically, paying this state tax at the entity level allows the Shareholder to deduct such tax against his or her federal taxable income, whereas much of the deduction otherwise would be lost at the individual level.[9]

IRC Section 338(h)(10) Election

If Buyer and Seller jointly agree, an IRC Section 338(h)(10) election would allow Seller to pay one level of tax (here, because the Company is an S corporation). This is because Seller is treated as selling stock for legal purposes, and treated as having the Company sell its assets for tax purposes.

Mechanically, the Company is treated as: (i) selling its assets to a new C corporation (“NewCo”), and (ii) liquidating and distributing the sales proceeds to Shareholder. Buyer is treated as acquiring stock of NewCo, except critically, NewCo has a stepped-up tax basis in the assets of the Company, allowing for additional depreciation and amortization deductions.

Shareholder is still taxed at ordinary income tax rates on the sale of certain assets (inventory, accounts receivable (if the Company is a cash-method taxpayer), and depreciation recapture), which is less favorable than a pure stock sale, but Buyer inherits the old tax liabilities (if any) of the Company, as well as the legal liabilities of the Company. Shareholder may mitigate the state tax burdens from the deemed asset sale by making a PTET election. The tax consequences to Shareholder under the IRC Section 338(h)(10) election are essentially the same as an asset sale (and as we will see, an F Reorg. followed by a sale of a newly created LLC). However, Shareholder and Buyer will need to ensure that the election is available under state law (not all states follow/conform to the IRC). Further, liabilities for taxes of the old Company will become the responsibility of Buyer, which is a legal distinction from a pure asset sale.

Tax Modeling is Critical

Shareholder is strongly recommended to engage a qualified tax professional to model the tax consequences of the stock sale versus the asset sale (with a PTET election made, if possible) in order to determine the after-tax cash difference between the two main structures, as well as any variants. This takes time and attention. It may require making certain assumptions, but is one of the surest ways Shareholder can potentially increase after-tax cash by comparing one structure to another.

A comprehensive model will show how much tax is paid under each structure. Such model allows the Shareholder to negotiate for additional cash consideration, perhaps pursuant to a gross-up mechanism, for any additional tax paid by the Shareholders under an asset sale or deemed asset sale. As mentioned, the asset sale or deemed asset sale is common so that Buyer can received a step-up in tax basis of the acquired assets.

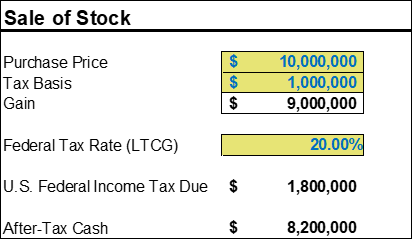

Seller Tax Model [10]

For illustration purposes, see the following table showing how the sale of stock will be treated given the following assumptions and calculations (excluding state taxes and NIIT). If the purchase price of Shareholder’s business is $10 million, and Shareholder had $1 million of tax basis in the Company stock, and assuming the holding period for long-term capital gains is met, the calculation of gain from a pure stock sale should look as follows:

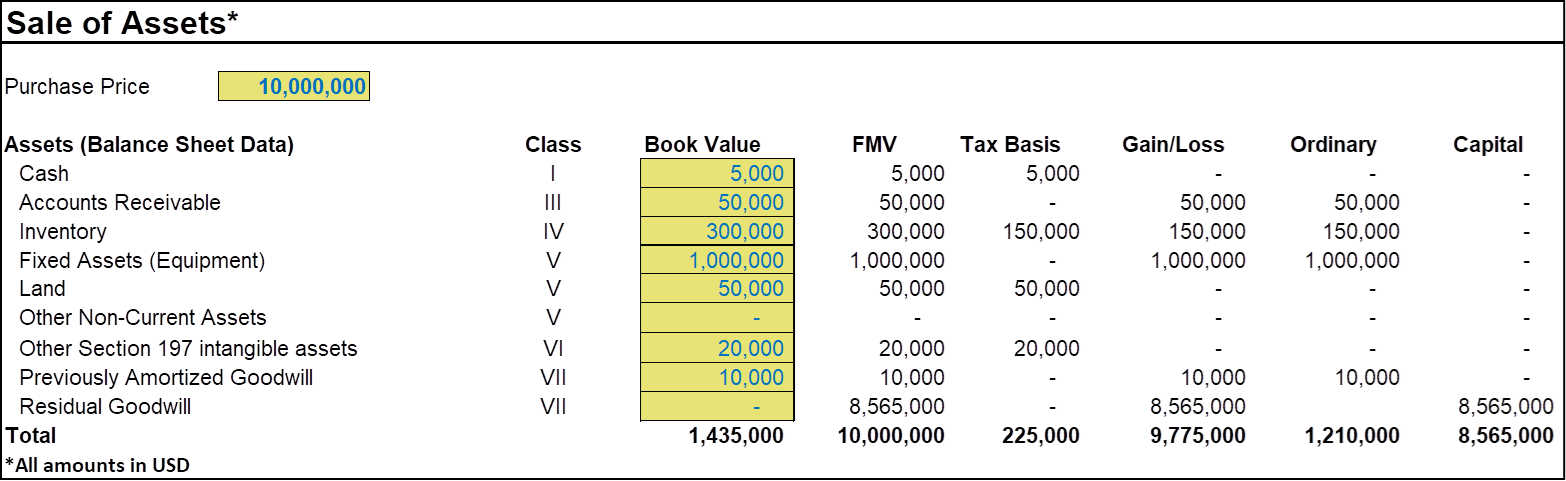

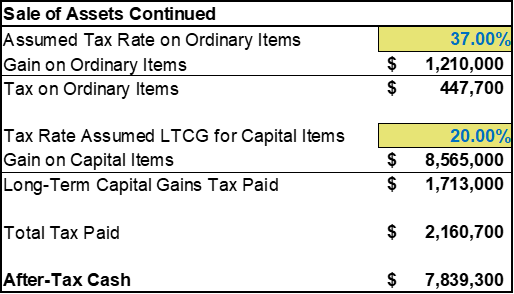

What about the sale of assets? This is a more complicated tax exercise. IRC Section 1060 instructs both the Buyer and Seller to allocate the total tax consideration among seven asset classes, Classes I – VII based on relative fair market value. The Seller then determines the Company’s tax basis of each class, and based on the allocation of tax purchase price to each class, determines the total gains and losses on all of the assets.[11] Any residual purchase price after allocating purchase price to Classes I through VI is allocated to Class VII assets. For simplicity, we assume that no PTET is paid by the Company, the balance sheet is stated as below, the taxpayer has no tax basis in accounts receivable and has fully-depreciated PP&E/fixed assets. We also assume the fair market value of the inventory has appreciated. Further, we assume that none of the fixed assets are taxed at the 25% tax recapture rate generally for certain depreciable real property, and that all ordinary items are taxed at 37%. We also did not depict state and local taxes or any NIIT.[12]

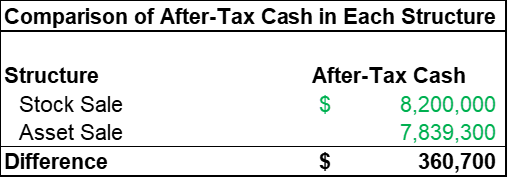

Based on the facts and assumptions in these models, Seller’s after-tax cash in an asset sale is $7,839,300 versus $8,200,000 in a stock sale.

This is clearly an oversimplification, but based on these models, Shareholder takes home $360,700 more in after-tax cash in a stock sale versus an asset sale, solely due to U.S. federal income taxes.

Further note, that if a 338(h)(10) election is made, the “Sale of Assets” model is more complicated.

Buyer Tax Model

Buyer should create its own model that should calculate the present value of deductions resulting from a step-up in tax basis for all applicable depreciable and amortizable assets, including goodwill, should they buy assets. After obtaining the present value of the additional deductions, Buyer then multiplies it by its expected effective federal and state and local income tax rate to determine the post-tax economic value of those deductions. Often times, if a shareholder insists on selling stock, a purchaser will attempt to require a downward adjustment to the stock price to reflect Buyer’s loss of a step-up. Note that in a stock acquisition, Buyer still receives carryover tax basis in the assets, and continues to depreciate or amortize those assets over their useful lives. So the difference between the continued depreciation and amortization, and the stepped-up depreciation and amortization deductions needs to be analyzed.

Buyer’s Responsibility for Seller’s Tax Liabilities in Each Structure

The structure of the transaction will impact the extent that the Buyer will take on liability for Seller’s U.S. federal income tax liabilities.

Stock Sale

As previously referenced, if the transaction is structured as a stock purchase, Buyer will acquire Company subject to any historical U.S. federal income tax liabilities. Because S corporations are passthrough entities, from a U.S. federal income tax perspective, there is less risk of entity-level income taxes unless the Company or its shareholder violated the rules for S corporation eligibility. In that case, the IRS could argue that its S corporation status should be revoked retroactively (and it would owe corporate income taxes).

Asset Sale

Again, in an asset sale, federal income tax liabilities of the Company should not be borne by the Buyer. State bulk sales notification laws may make Buyer responsible if notification requirements are not met; however, the purchase agreement will likely require that Seller indemnify Buyer for these pre-closing state tax liabilities.

338(h)(10) Deemed Asset Sale

The Treasury Regulations expressly provide that NewCo, which Buyer is deemed to acquire, will be responsible for any U.S. federal tax liabilities of OldCo.[13]

Other structures will offer Buyer different levels of protection from U.S. federal tax liabilities. These include: (i) a pre-closing F reorganization followed by a conversion of the Company to an LLC and sale of the Company’s membership interests; and (ii) an asset drop down to a new single-member LLC and sale of those membership interests.

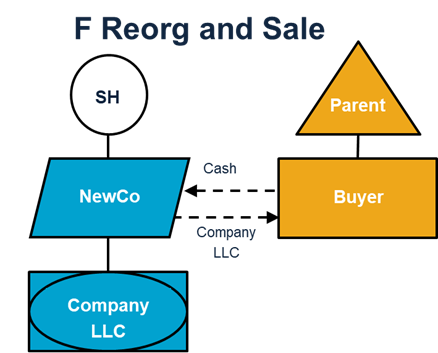

F Reorganization, followed by a Conversion and Sale of Membership Interests

This transaction is widely used and requires additional compliance and corporate structuring. In this structure, prior to closing, Seller will engage in several steps to complete an F reorganization (the “F Reorg.”). Critically, Treasury Regulation Section 301.7701-2(c)(2)(iii)(A)(1) impinges on Buyer’s goal of not inheriting historical tax liabilities of the Company in most cases.[14]

Thus, it may not make sense for Buyer to push for an F Reorg. structure if the primary goal is to avoid the transfer of the Company’s tax liabilities.

If the primary goal for Buyer is to achieve a step-up in tax basis, the F Reorg. is a viable option (albeit other alternatives discussed may be simpler).

The steps to an F Reorg. are as follows:

- Shareholder forms NewCo, a C corporation, and obtains an EIN for NewCo;

- Shareholder contributes all of the Company stock to NewCo;

- NewCo makes a Qualified Subchapter S election for the Company by filing Form 8869, which will: (i) convert the Company into a QSub, which is treated as a disregarded entity for federal income tax purposes (just not under the check-the-box rules); and (ii) by virtue of that being treated as an F reorganization under IRC Section 368(a)(1)(F), convert NewCo to an S corporation;

- The Company then converts to an LLC by filing a certificate of conversion with the applicable state corporate office (e.g., Secretary of State); and

- NewCo then sells the Company’s membership interests to Buyer.

Here is what the final steps and sale would look like:

Buyer will be treated, for U.S. federal tax purposes as acquiring all of the Company’s assets and will receive a stepped-up tax basis in such assets.

NewCo is treated as selling assets, and the character of gain on such assets will flow through to Shareholder. Note that there are several tax forms, steps, and legal documents that need to be drafted and agreed to for the F Reorg. to take place.

We recommend the parties budget at least a week to complete the F Reorg. and sale, and all sides should review the tax forms and legal documents in order to ensure a good F Reorg. In some instances, we have seen Buyer pay for the pre-transaction reorganization documentation because Buyer is receiving the step-up in tax basis.

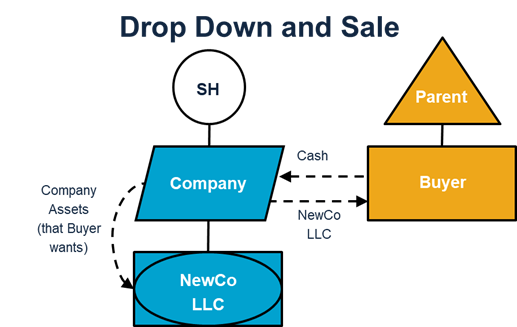

Actual Drop Down of Assets to a New LLC

One structure that should protect Buyer from assuming any U.S. federal tax liabilities is to arrange for the Company to contribute its assets to a new limited liability company, and then Buyer purchases those assets, or the membership interests of the LLC, for cash.

This structure may not be feasible to the extent that the need to retitle assets becomes complicated or restricted, the degree to which notices need to be provided to creditors, or the extent to which potential transfer taxes are triggered. However, if it’s available, and Buyer acquires 100% of the membership interests in the new LLC, Buyer is deemed to acquire and the Company is deemed to sell assets for U.S. federal tax purposes.

Added Benefit of F Reorg. or Actual Drop Down

One added benefit of the F Reorg. or drop-down structures above is that they allow for the selling company to retain unwanted assets. With an F Reorg., because the newly created LLC is a disregarded entity, assets that the Buyer has no interest in can be distributed up to NewCo with no tax consequences. Such a structure may also avoid bulk-sales notifications, depending on the state law of whether or not the sale of membership interests creates a bulk sale filing requirement, versus a true asset sale and acquisition.

To the extent that Buyer wants Seller to continue to own an interest in the Company, Buyer may request that Seller, post F Reorg. or post Drop Down, make a direct contribution to the NewCo or Company LLC and spring that entity to life as a partnership. The partnership then makes an IRC Section 754 election, and when Buyer acquires membership interests in the target, it receives a stepped-up tax basis in the underlying interests of the partnership assets it acquires because of the Section 754 election. This can be a tax efficient way to structure a rollover.

Reporting the Tax Consequences of the Transaction

Asset Sale and Acquisition

IRC Section 1060 applies when there is an applicable asset acquisition. An applicable asset acquisition is defined as any transfer of assets which constitutes a trade or business in the hands of a buyer or seller. IRC Section 1060 also applies to purchases of single-member LLC’s and partnership interests. When a partnership interest is transferred, see Treas. Reg. §1.755-1(d).

What happens when IRC Section 1060 applies? The parties will file IRS Form 8594 (each party files their own form attached to its annual income tax return), and the parties will allocate the purchase price (e.g., cash paid and liabilities assumed) to each class of assets based on the FMV of each asset, with the residual fair market value allocated to goodwill (Class VII). There are several key considerations here for both parties.

Hot Assets

Shareholder will want to minimize the allocation of purchase price to assets such as inventory, accounts receivable, and depreciable equipment. Obviously, this is because Shareholder will recognize ordinary income on the sale of appreciated inventory, accounts receivable (if on the cash-method) and depreciation recapture.

Buyer would like to allocate purchase price to property with faster recovery lives such as inventory and equipment. Doing so may allow Buyer to offset inventory costs against sales income or take bonus depreciation, in both cases reducing its taxable income the first year after acquiring the assets. So there will be a negotiation between the Buyer and Seller as to the agreed-upon fair market value of the assets for purposes of the Section 1060 allocation.

Non-Competes

Another key item here is how to treat covenants not to compete. Covenants not to compete are a Class VI intangible, but more importantly result in the recognition of ordinary income to the Shareholder. Form 8594 specifically asks if the transaction is subject to a noncompete, license, lease, employment management contract or similar agreement, and asks that a separate statement be attached describing the type of other agreement entered into and the maximum consideration allocated to such other agreement.

While there is no legal requirement that the parties agree on an allocation or file matching Forms 8594, most purchase agreements include provisions that the parties will agree to a purchase price allocation among the classes of assets consistent with IRC Section 1060, who will control the allocation, and how much will be allocated to each class perhaps with the use of an indicative schedule. As far as timing, the instructions provide, “Generally, attach Form 8594 to your income tax return for the year in which the sale date occurred. If the amount allocated to any asset is increased or decreased after the year in which the sale occurs, the seller and/or purchaser (whoever is affected) must complete Parts I and III of Form 8594 and attach the form to the income tax return for the year in which the increase or decrease is taken into account.”

Deemed Asset Acquisition – IRC Section 338(h)(10)

Form 8594 is not required when an IRC Section 338(h)(10) election is made by the parties. Instead, IRS Forms 8023 and 8883 must be filed.

Form 8023 is the actual 338 election form itself, which is signed by both parties.

Form 8883 includes Part V, which contains a similar asset allocation table to that mentioned above on Form 8594. Form 8883 is filed by OldCo. (the Company) and NewCo. (presumably, Buyer on behalf of the Company). Form 8883 does not contain a separate statement/question regarding noncompete agreements.

For timing, the forms are attached to the return on which the effects of the IRC Section 338(h)(10) deemed sale and purchase of the target’s assets are required to be reported (e.g., the Company’s last tax return as an S corp. when it’s owned by Shareholder, and the Company’s first tax return when it’s owned by Buyer).

Key Takeaways

If you are selling your S corporation business, there are a number of different structures available by which the transaction can be effected, with different general corporate law and tax implications. Except for perhaps single-asset entities, Sellers would be well-advised to engage a qualified tax professional who is experienced in representing sellers to help structure the sale and develop a tax model so that a seller can see the federal and state income tax implications of different structures. A good tax model will demonstrate the after-tax cash to Seller of a stock sale versus an asset sale (or versus a deemed asset sale under IRC Section 338(h)(10) or otherwise). An experienced and qualified tax professional will explain the best structure to navigate the transferring of tax liabilities and help negotiate the purchase price on your behalf.

The structure, deal terms, timing, indemnification provisions, and numerous other provisions need to be captured in the purchase agreement to ensure a tax-efficient outcome.

Should you have any questions or comments on these topics, please contact the author or any attorney with the firm’s Tax Practice Group. You can also visit our Tax Law Defined® Blog for more insight into the latest developments in federal, state and local tax planning and tax administration.

Appendix I – Tax Shapes

The information provided in this article does not constitute legal advice (and should not be relied on by any individual or entity as such) and does not create an attorney-client relationship. Its intention is to merely be informative and help advisors and taxpayers understand the law and the options therein.

[1] The information provided in this article does not constitute legal advice and does not create an attorney-client relationship.

[2] Sellers of an S corporation will likely need to provide the last three-years of tax returns (federal and state) to a buyer during due diligence. Be sure to have all documentation and support for tax positions ready in advance, as dubious positions can result in a reduction of purchase price (in the event of audit or otherwise).

[3] This article includes tax shapes to help depict what is happening. See Appendix 1 for a key of what each shape means (“SH” is the Shareholder).

[4] If the taxpayer is active in the trade or business and materially participates, as described in the Internal Revenue Code and regulations, the NIIT should not apply in part because the Company is assumed to be a pass-through entity.

[5] Note that because Buyer is not a qualified S corporation shareholder under the Internal Revenue Code, the Company’s S status will terminate upon sale to Buyer, and so the Company would become a C corporation for U.S. federal income tax purposes beginning the day of closing. See IRC Section 1362(d)(2)(B). The S corporation would have a short taxable year ending the day before the sale, and would be a C corporation from the closing date to the end of the tax year. If a Section 338(h)(10) election is applicable, under Treas. Reg. Section 1.338(h)(10)-1, “[w]hen T is an S corporation target, T’s S election continues in effect through the close of the acquisition date (including the time of the deemed asset sale and the deemed liquidation) notwithstanding section 1362(d)(2)(B).”

[6] As indicated, the good news for the Shareholder is that the Company has the cash proceeds from the sale, and will likely distribute the cash to the Shareholder in a transaction that should not result in gain to the Shareholder. There should not be a second level of taxation. This is distinguished from the tax consequences if the Company were a C corporation. We are assuming that no built-in gains tax under IRC Section 1374 applies to the Company’s asset sale. This primarily assumes that the Company has been an S corporation for at least five years (or since its inception).

[7] If the Company is on the accrual method for federal income tax purposes, it should have tax basis in its accounts receivable. If the Company holds inventory that has appreciated, the gain recognized on the sale of such inventory is treated as ordinary income. Some items of depreciation recapture of certain real estate are taxed at 25%, versus the 37% rate pursuant to IRC Section 1(h)(1)(E). Gain or loss from the sale of IRC Section 1231 property (property used in a trade or business that is held for more than one year) is separately stated and flows through to the Shareholder. Note that if the Shareholder has a net IRC Section 1231 gain on the year, he or she may have long-term capital gain. If the Shareholder has a net IRC Section 1231 loss on the year, such loss is ordinary. Note that recapture income recognized under IRC Sections 1245 and 1250 will be treated as ordinary income despite IRC Section 1231.

[8] In New Jersey, this is often referred to as the Business Alternative Income Tax (“BAIT”) election.

[9] See generally, IRC Section 164(b)(6). Business owners should be aware of the PTET election and should talk to their tax advisors about such election.

[10] The models in this article are for illustrative purposes only and cannot and should not be relied on as tax or legal advice or creating an attorney-client relationship.

[11] Treas. Reg. Section 1.1060-1(c)(2) incorporates by reference Treas. Reg. Section 1.338-6, which describes classes I – VII. Taxpayers can also look at the instructions for Form 8594 for such asset classifications.

[12] To complete this exercise, most taxpayers use a current balance sheet, and make adjustments to get to tax basis and fair market value of the various assets.

[13] See Treas. Reg. Section 1.338-1(b)(3).

[14] Effectively, this regulation means that if the S corporation was a “bad S corporation,” due to an ineffective S corporation election or violating the S corporation rules, it will have been a C corporation for tax purposes in the past and owe corporate income tax. As such, performing the F Reorg. will not cleanse Buyer for historical tax liabilities of Company LLC. Thank you, J.R.P.